Case Study · Product Design

Reducing Risk

Freeze Rates

Using empathy to reduce new seller churn by 4% and risk freeze rates by 16%

Case Study · Product Design

Using empathy to reduce new seller churn by 4% and risk freeze rates by 16%

Background

Square's Risk team relied on a combination of automated and human systems to protect the platform and its users from fraud. But by 2024, those same systems were increasingly catching good sellers in the crossfire, driving up seller complaints, lengthening risk resolution times, and ultimately accelerating GPV churn.

My team focused on services sellers: landscapers, contractors, photographers, and other businesses that sell their time and expertise. The nature of their work means they often process infrequent, high-value, card-not-present transactions, which is also exactly what fraud looks like. As a result, services sellers were being risk-actioned at more than twice the rate of any other seller group on Square, and we believed that experience was a leading driver of churn among new sellers.

My team was brought in on a special engagement to collaborate with the Risk team to find ways to reduce the negative impact of risk actions on sellers without exposing Square to more risk losses.

Process

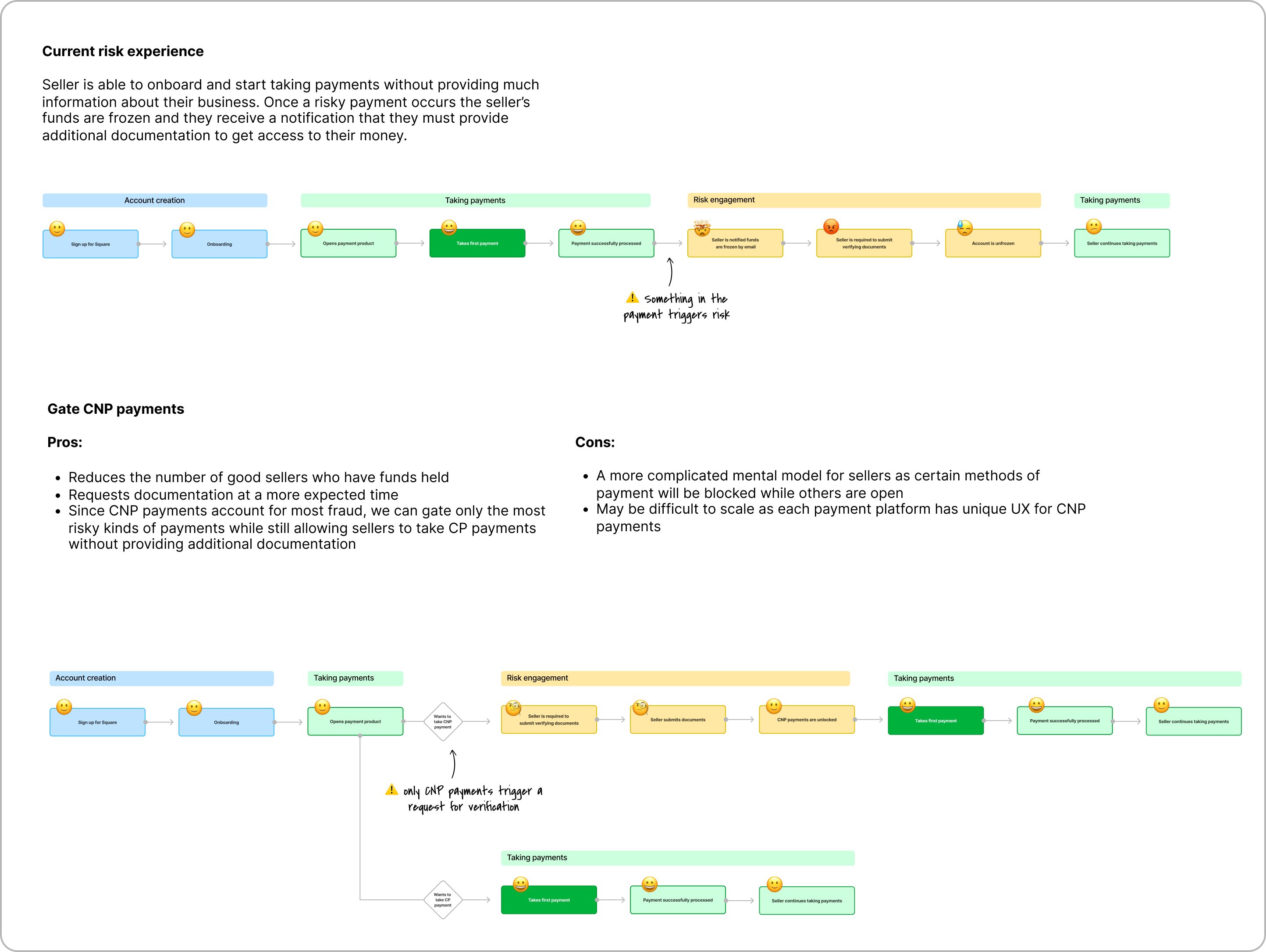

While other teams focused on improving risk model accuracy and refining how risk actions were communicated, my team was tasked with specifically tackling fake account risk actions. These occur when Square suspects a seller may not be who they claim to be, resulting in frozen funds until the seller provides identifying documentation. These freezes were responsible for 93% of GPV churn. As we explored how to reduce this impact, we identified that the timing of when we request these documents presented the biggest challenge, and framed it as a two-part "Goldilocks" problem.

Good sellers expect Square to verify their identity in a way that won't interfere with access to their funds, and at moments that feel natural. Verifying too late, after a seller has already completed onboarding and begun processing payments, creates frustration, confusion, and ultimately churn.

The earlier we try to prevent fraud, the fewer signals we have to distinguish good actors from bad. Verifying too early risks creating friction that hurts activation or payment conversion rates. An experiment requiring 100% of sellers to upload identity documents before taking payments resulted in even worse damage to bottom-of-funnel metrics.

Seller Feedback

"Pretty upset that my account has been in review for over a week with almost $3,000 completely untouchable... I've had my account for only a month."

SMB Seller, Photography

"These reviews have caused severe financial strain for my business at times, to the point that I have strongly considered discontinuing the use of Square."

Micro+ Seller, HVAC Repair

"Secondly you're holding my funds for over a month to verify me. That is unacceptable considering when you set up your app and give your information you should have asked for it up front."

SMB Seller, Landscaper

Our hypothesis: We can reduce risk-based churn by optimizing when we request identity documents, placing them where they better match seller expectations and reducing the likelihood that accounts need to be frozen.

During discovery, we found that the transactions most likely to trigger fake account risk actions were card-not-present (CNP) payments, where the seller manually enters a credit card number or the buyer pays remotely via something like an invoice. These accounted for over 75% of transactions that triggered risk actions, so by focusing on CNP payments specifically, we could target the transactions most likely to result in account freezes.

We also knew that 80% of fake account freezes occur after a seller's first or second payment, meaning any effective intervention needed to happen as early in the seller journey as possible.

We audited CNP payments across all payment platforms including Invoices, Virtual Terminal, and the Square POS. Ultimately, due to internal constraints around testing timelines and mobile eng resources, we aligned on a proof of concept that focused on the web-based payment platform Virtual Terminal only. If we saw a positive impact from this small, segmented test, then we could justify further investment to scale it across other platforms.

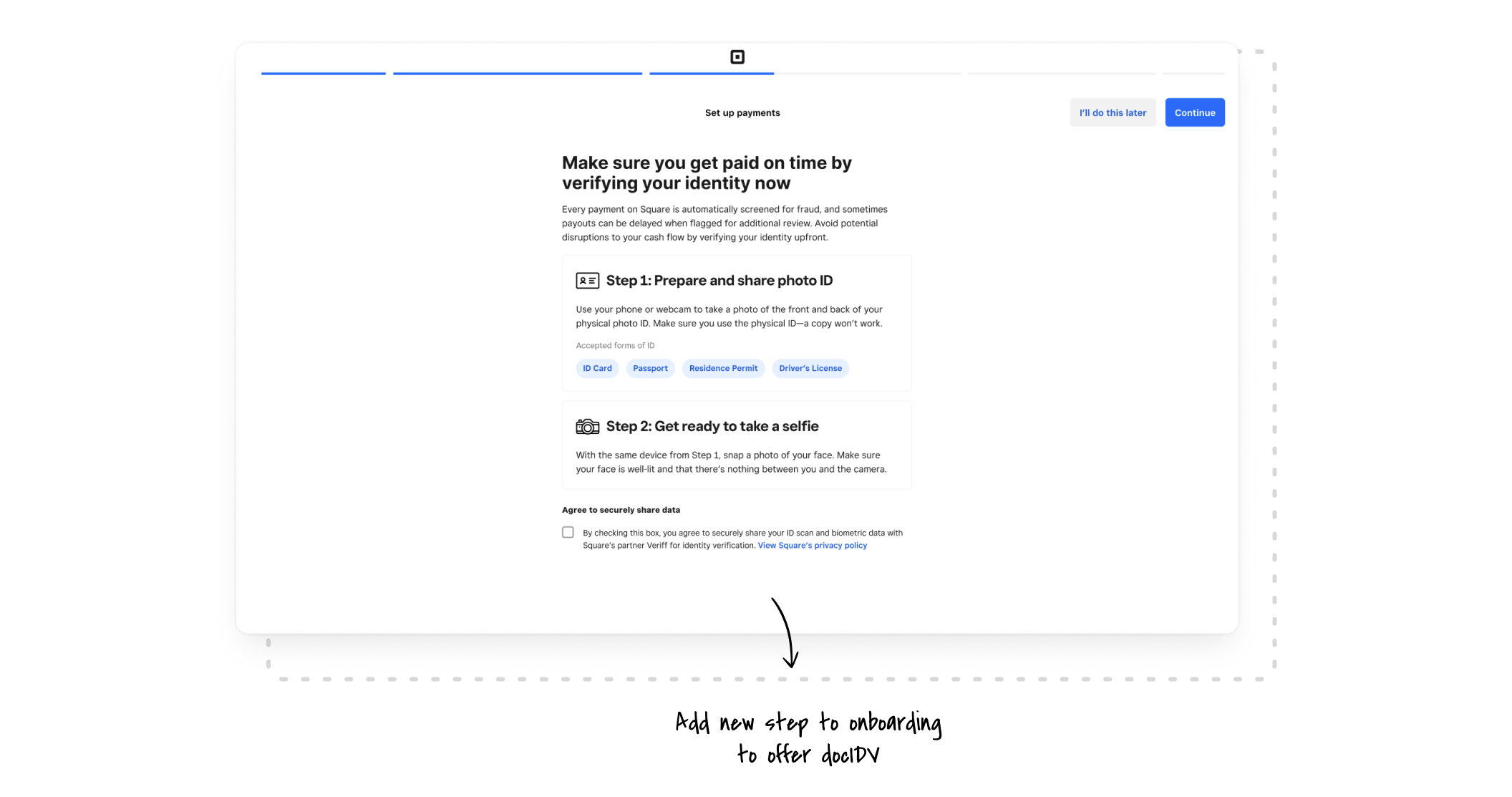

A key moment came while mapping out the seller experience with gating. I advocated that, for an optimal user experience, we needed to give sellers the option to do DocIDV prior to encountering blocked payment methods. We knew there was a high likelihood for confusion or frustration during the initial payment flow when sellers realized not all payment methods were accessible. I felt that sellers would be more understanding if they had already been given the choice and declined, and that we could get more sellers to complete verification proactively, avoiding the gate entirely.

Research

Once we had aligned on the approach, we wanted to get feedback from sellers on the proposed gating experience. As CNP vs CP payment methods are not intuitive distinctions for sellers, we knew it would be a challenge to clearly explain which payment methods were and weren't available to them. We also wanted to stress test how sellers would react to having an initial payment experience disrupted in this way.

Using the scenario that the seller had just signed up for Square and skipped an optional ID verification step, we tested a simple, single prototype. The prototype took the 8 sellers (4 Square sellers, and 4 non-Square sellers) from the VT dashboard through an ID verification modal and finally to a gated version of VT.

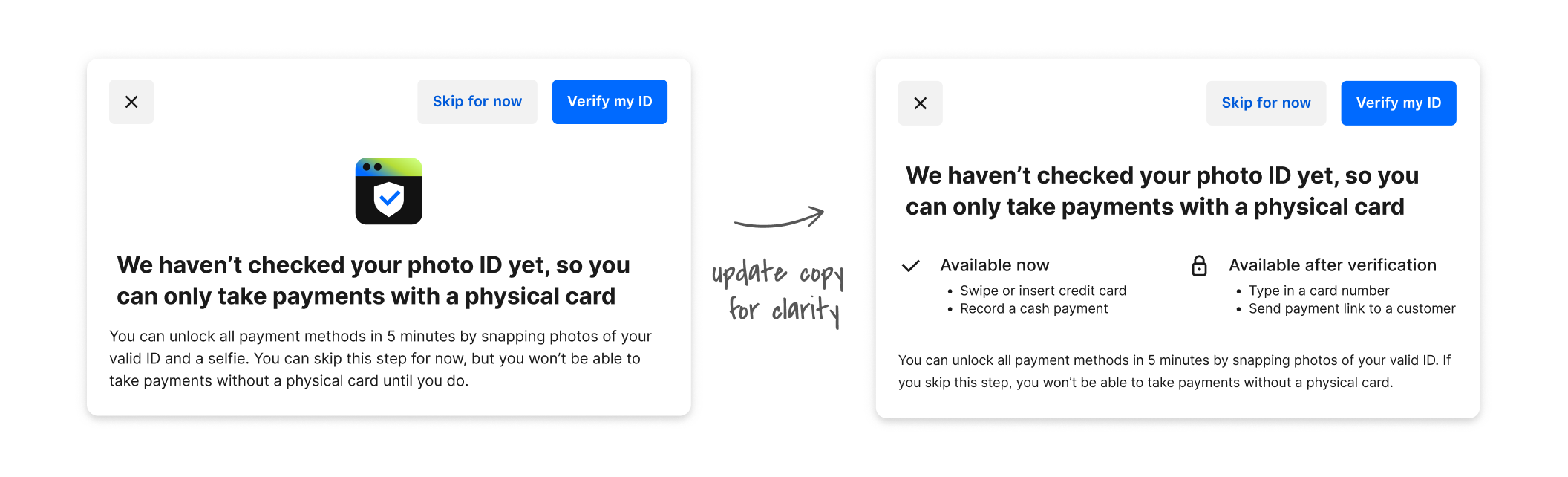

Overall, the prototype was a success. We found that sellers were understanding and appreciative of the security rationale for blocking certain kinds of payments. However, they did want more explicit information around what payment types were available pre and post verification to help them decide if they wanted to move forward with DocIDV in that moment.

Research Recommendations

Sellers wanted explicit information around which payment types were available before and after verification. The modal needed to clearly list what was blocked and what would be unlocked to manage expectations for what they would see next.

"The screen doesn't specify I'm going to have other options"

"You told me I'm not allowed more, but I have these other options. I should have been told that on the previous screen."

"I don't know what the other payment methods are"

A key takeaway that validated earlier instincts was that giving sellers an opportunity to complete identity verification prior to the payment moment (during initial onboarding) was vital to reducing seller frustration when they encountered the gate.

"I should have done [verified my identity] when you originally asked me to."

"Obviously [not being able to take payments] would be frustrating, but I'm the one that chose to skip that step."

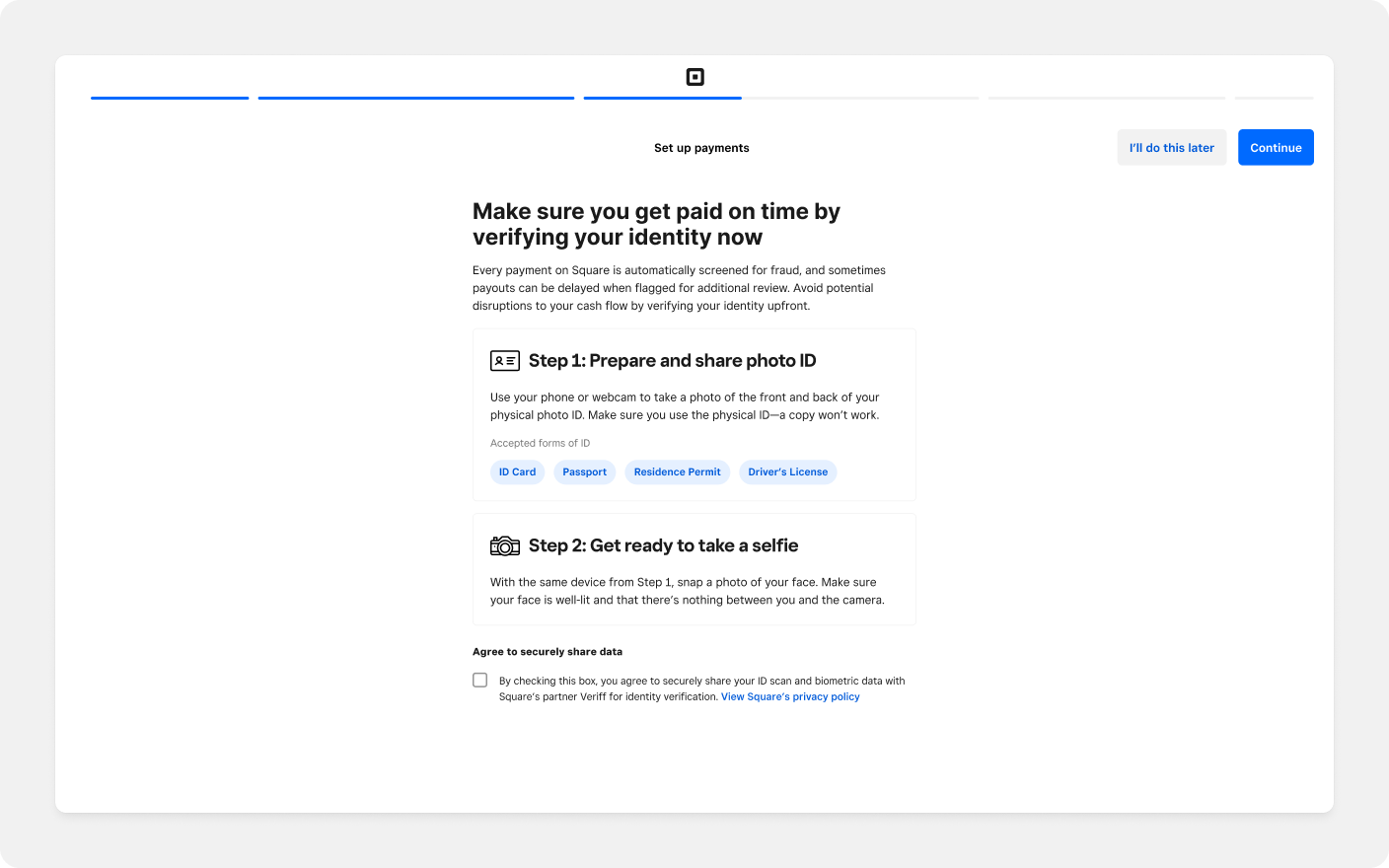

Solution

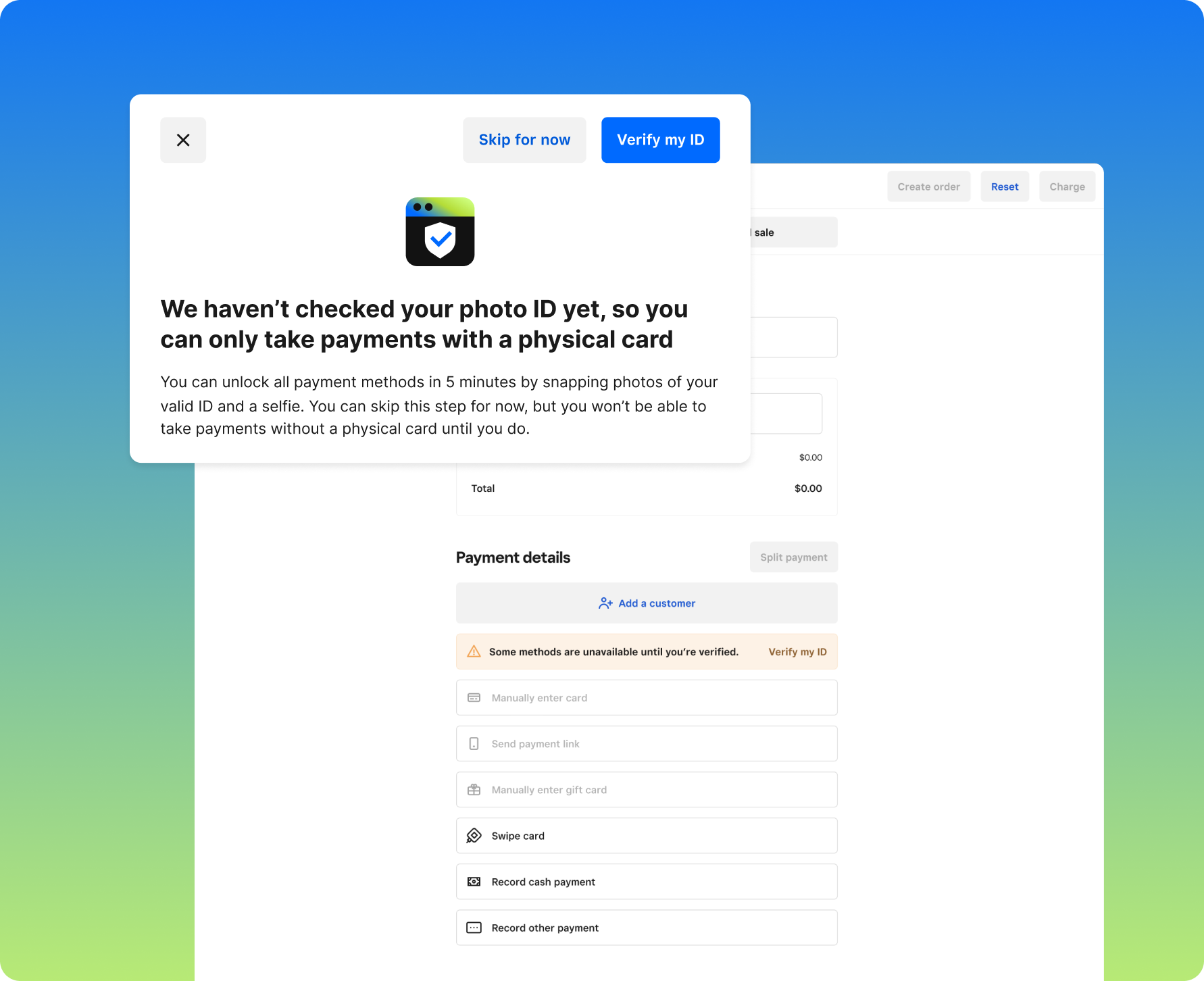

All sellers are shown a screen during payment setup where they can choose to complete document identity verification (DocIDV). We updated the headline and subheading to clearly explain the benefit of completing the step at this point in the process and what would happen if the seller chose to proceed without doing it.

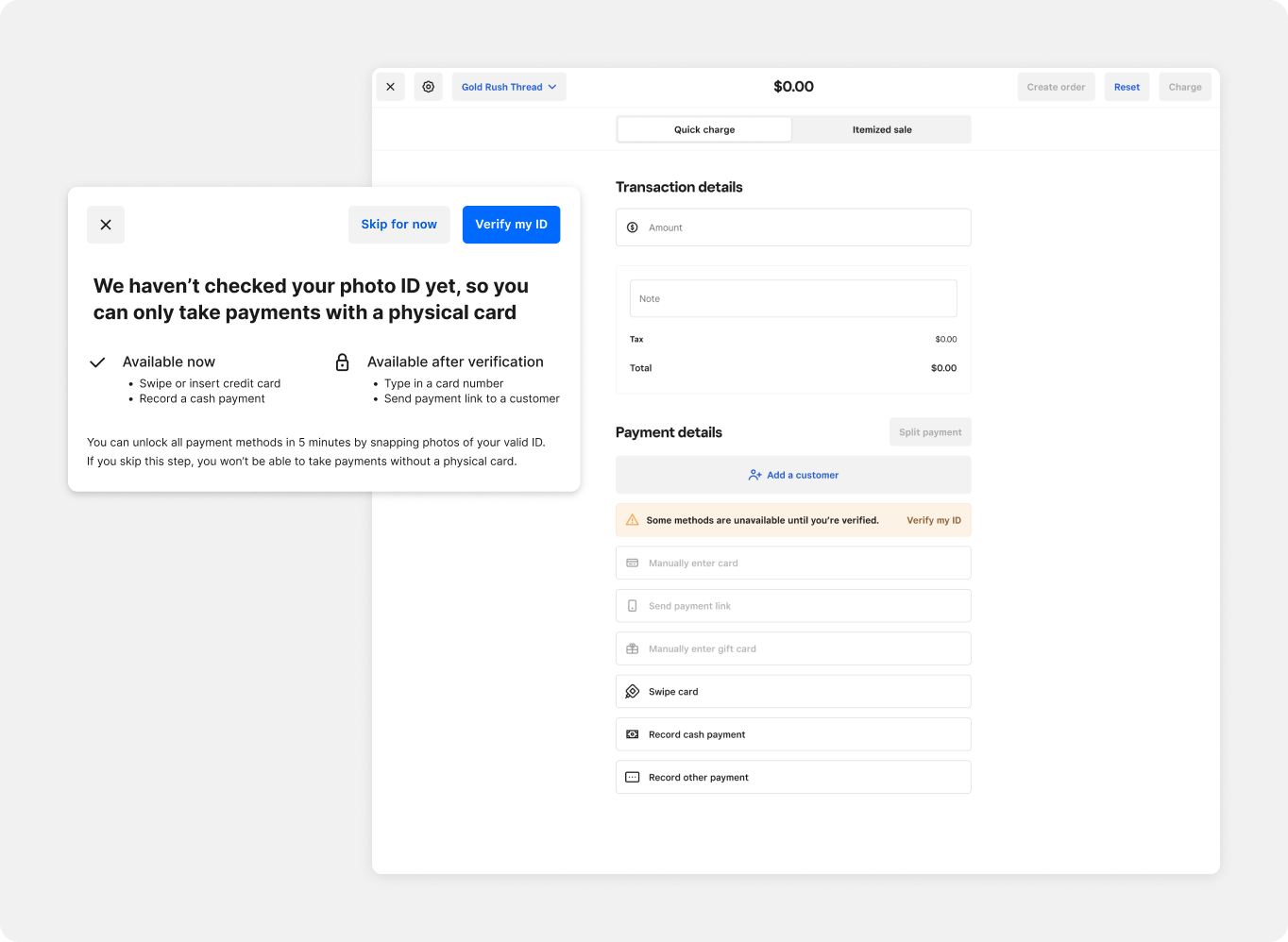

Sellers who skip verification during onboarding will not be able to take CNP payments when they navigate to Virtual Terminal. They are warned of this via a modal when they click on the take payment CTA. The modal explicitly lists which payment methods are available now vs. after verification, directly addressing the usability testing insights.

Success despite eng limitations

When the team got to eng implementation, we discovered that eng support had been reduced and that the gating mechanism would take twice as long to build as originally planned. The entire project was suddenly at risk. However, we found that we did have bandwidth to still proceed with the optional docIDV alone, without gating any payments later.

This empathy-driven design decision alone drove a massive decline in freeze rates and an actual reduction in new seller churn. This was one of the team's highest impact interventions to date.

Scaling the solution

As a result of the success, in 2026 we scaled the intervention to include a "second chance" DocIDV flow to allow sellers who skipped verification to go back and complete the step, and a mobile-native version of DocIDV that allowed scaling the proactive DocIDV experience to iOS and Android.